The Charles Lucius most people are searching for is Charles E. 'Chuck' Lucius, the founder and CEO of blank" rel="noopener noreferrer">Gradient Investments, LLC, a Minnesota-based SEC-registered investment advisory firm. Based on publicly verifiable ownership disclosures and a reasonable analysis of the firm's assets under management, the most credible estimate of his net worth as of 2026 sits somewhere in the range of $5 million to $15 million, with a central estimate around $7 to $10 million. That range reflects real uncertainty, not laziness, and I'll walk you through exactly why below.

Charles Lucius Net Worth: Estimate, Sources, and Breakdown

Derek Mansfield

1 Jun 2026

First: Which Charles Lucius Are We Talking About?

The name Charles Lucius turns up in a few different contexts, so it's worth being direct about who this article is about. There's at least one Charles Lucius listed as an author in literary catalogs, another appearing as a volunteer organization president in a 2026 community directory, and a LinkedIn user profile under the same name. None of those are the person generating the most financial-interest searches.

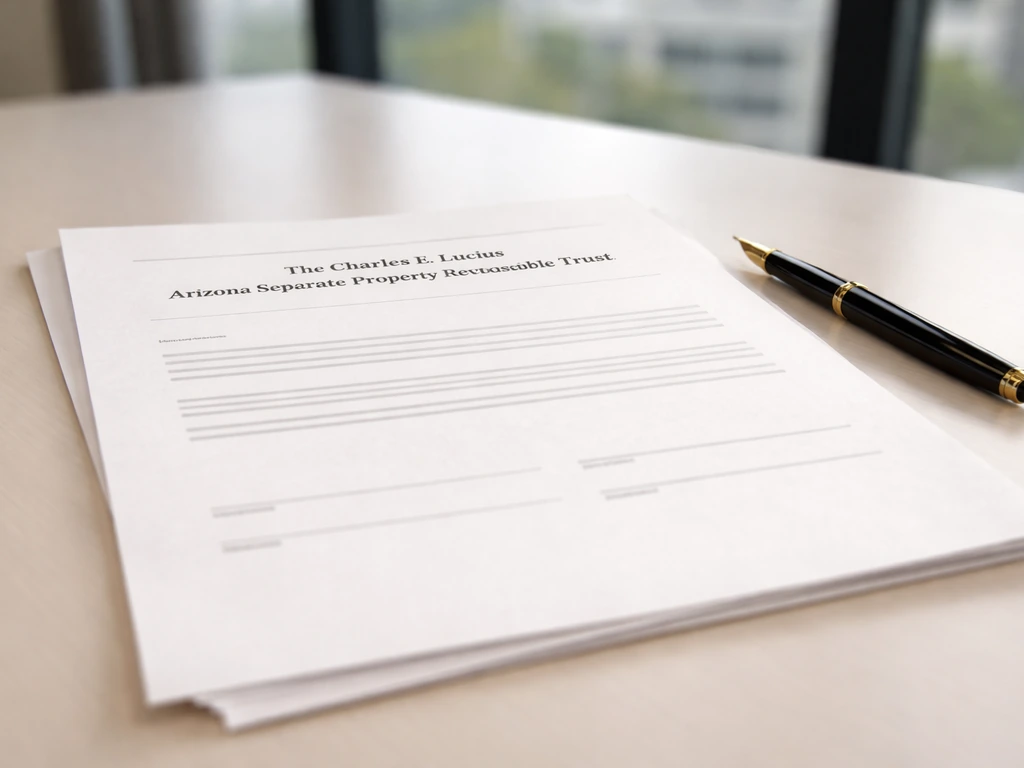

The financially relevant individual is Charles E. Lucius, registered with FINRA under CRD number 1012912. He's verifiably tied to Gradient Investments, LLC (CIK 1542265 in SEC records), an independent, privately-owned registered investment adviser based in Arden Hills, Minnesota. His ownership stake is documented in the firm's Form ADV disclosures, specifically through an entity called 'The Charles E. Lucius Arizona Separate Property Revocable Trust,' which holds an 80% ownership interest in Gradient Investments. That's the Charles Lucius this article covers.

The Net Worth Estimate and How Confident We Should Be

One site, Worth Collector, puts Charles Lucius's net worth at approximately $7 million. That's a reasonable ballpark, but it arrives without a transparent methodology, so treat it as a starting point rather than a conclusion. My own estimate, derived from the income and ownership inputs below, puts the range at $5 million to $15 million, with moderate confidence.

| Factor | What We Know | Confidence Level |

|---|---|---|

| Firm ownership stake | 80% owner via revocable trust (Form ADV) | High — regulatory disclosure |

| Firm AUM | Approximately $8.2 billion (SmartAsset, 2025 data) | High — reported figure |

| Personal net worth estimate | $5M to $15M range, ~$7M–$10M central estimate | Moderate — inferred, not confirmed |

| Salary or direct compensation | Not publicly disclosed | Low — private firm |

| Personal investment holdings | Not separately filed or disclosed | Low — no public 13F at personal level |

The honest answer is that because Gradient Investments is a privately held firm, there's no public salary filing, no stock option disclosure, and no personal balance sheet to pull from. What we have is an ownership stake in a company managing over $8 billion in client assets, a career spanning several decades in the financial services industry, and regulatory filings that confirm the structure of that ownership. From those inputs, a seven-figure net worth is credible. Eight figures would require assumptions about fee revenue and margin that aren't documented publicly.

How This Estimate Is Actually Calculated

When there's no celebrity paycheck or public stock holding to point to, estimating net worth becomes a process of working backward from what's disclosed. Here's the approach used for Charles Lucius specifically.

AUM-Based Revenue Inference

Gradient Investments manages approximately $8.2 billion in assets under management. Registered investment advisers typically charge advisory fees in the range of 0.25% to 1% of AUM annually, though institutional and wrap-fee structures can push that lower. Even at a conservative blended rate of 0.20% to 0.30%, the firm's gross revenue would land somewhere between $16 million and $25 million per year. As an 80% owner and CEO of a fee-only firm, Charles Lucius's share of profits after operating costs would represent a meaningful portion of that. Over time, accumulated savings, reinvestment, and compounding would build into a significant personal estate.

Equity Value of the Firm Itself

Independent RIA firms are frequently valued at 2x to 3x annual revenue for acquisition purposes, sometimes higher for high-growth practices. If Gradient's revenue is in the $16 million to $25 million range and a buyer would pay 2x to 3x that, the firm itself could be worth $32 million to $75 million. Charles Lucius's 80% stake would theoretically be worth $25 million to $60 million in a sale scenario. However, this is a theoretical valuation, not liquid wealth. He hasn't sold the firm (at least not in any publicly disclosed transaction), so this represents potential, not current realized wealth. That's a critical distinction.

The Revocable Trust Structure

The fact that ownership is held through 'The Charles E. Lucius Arizona Separate Property Revocable Trust' is informative. A revocable trust used to hold business equity is a common estate-planning tool that keeps assets out of probate while retaining control. It also signals that this is long-held, intentionally structured wealth, not a recent windfall. Arizona separate property language suggests the trust may have been established to protect assets from marital property claims, which is a standard financial planning move at this wealth level.

Career Timeline and How the Wealth Was Built

Charles E. Lucius didn't start in the investment advisory world. Based on hedgefunddb's career narrative and FINRA BrokerCheck records, his career trajectory looks roughly like this:

- Early career in insurance: Lucius got his start at Prudential in insurance-related roles, building his understanding of financial products and client relationship management before transitioning to investment services.

- Brokerage leadership: He moved into leadership at Personalized Brokerage Services and later served as President and Principal at USAllianz Securities, accumulating credentials and a client base in the broker-dealer world.

- Founding Gradient Investments: He eventually launched Gradient Investments, LLC as an independent, fee-only registered investment adviser. This move from commission-based brokerage to fee-only advisory reflects a broader industry shift and also aligned his compensation model more directly with long-term firm growth.

- Growing to $8+ billion AUM: Gradient scaled significantly over the years to manage over $8 billion in client assets, which puts it among the larger independent RIAs in the country.

- Ongoing CEO and majority owner role: As of 2025 regulatory filings, Lucius remains the majority owner through his revocable trust, with CRD #1012912 still active.

The wealth-building story here is one of equity accumulation over decades rather than a single big exit or a public-market windfall. His education background includes an MBA and a bachelor's in marketing, along with industry certifications, which tracks with the career path described above. This is a profile of someone who built wealth steadily through firm ownership, fee revenue, and compounding, not someone who sold a startup at 35 and retired.

Assets, Investments, and Publicly Verifiable Financial Milestones

Because Gradient is a private firm, there's no IPO filing, no proxy statement, and no 10-K to pull. But here's what is publicly verifiable and financially relevant:

- 80% equity stake in Gradient Investments, LLC, held through a revocable trust and documented in Form ADV filings dated as recently as February 2025.

- Gradient Investments' reported AUM of approximately $8.2 billion, making it a substantial independent RIA by any measure.

- SEC registration and ongoing compliance filings, including 13F-HR filings from Gradient as an investment manager (visible in SECInfo and FilingExplorer), which confirm the firm's active status and scale.

- FINRA BrokerCheck registration under CRD #1012912, providing a verifiable career history including employment records and any regulatory disclosures.

- A revocable trust structure under Arizona law holding the majority equity, suggesting deliberate estate and asset protection planning consistent with multi-million-dollar wealth management.

What's not publicly available: personal real estate holdings, personal brokerage or investment accounts, any business sale proceeds, or specific annual income figures. If there have been partial equity sales to strategic partners or third-party investors (a common move for growing RIAs), those transactions would not be publicly disclosed unless they triggered SEC or FINRA reporting thresholds.

Why Net Worth Numbers Vary So Much Across Sites

If you've already searched around, you've probably seen figures that range from vague references to a few million dollars all the way up to speculative estimates that don't match anything in the public record. Here's why that happens, and how to read those numbers critically.

- Celebrity-style aggregators use formulas: Sites like Worth Collector apply generic estimation models based on job title, industry, and sometimes social media presence. These aren't wrong in principle, but they don't incorporate firm-specific data like actual AUM or equity structure.

- Private firm data is simply unavailable: Unlike public company executives whose equity is disclosed in SEC proxy statements, private firm owners like Charles Lucius have no equivalent obligation to publish personal wealth data. That creates a vacuum that different sites fill differently.

- AUM is not the same as personal wealth: A firm managing $8 billion does not mean its founder has $8 billion. It means the firm earns fees on that capital. Conflating the two is a common error in celebrity-style net worth content.

- Revocable trust ownership adds a layer of indirection: The ownership is held in trust, not personally. Some estimators treat this differently depending on how they interpret beneficial ownership.

- No single verified source exists: Even the Form ADV, the most reliable document available, discloses ownership percentages and firm structure, not the individual's personal bank balance or total asset picture.

The same pattern shows up across profiles of other financial professionals covered on this site, where the name 'Charles' connects to very different wealth stories depending on the industry and documentation available. A directory-style listing that includes “Charles E Lucius” (such as a SimpleContacts entry) can help with identifying the right person by location, but it is not authoritative for verifying wealth and should be corroborated with primary records directory-style listings that list different “Charles” profiles. The methodology here is the same: start with what's in regulatory filings, apply industry-standard revenue multiples, and flag the uncertainty clearly rather than pretending precision that doesn't exist.

How to Check for Updates and Spot Changes in the Estimate

Net worth estimates for private financial professionals like Charles Lucius can shift meaningfully based on a handful of triggers. Here's where to look and what to watch for.

Primary Sources to Monitor

- SEC AdviserInfo (reports.adviserinfo.sec.gov): Search for CRD #1012912 to pull the most current Form ADV and any updates to the ownership structure or AUM reported by Gradient Investments. This is your most reliable data point and it updates at least annually.

- FINRA BrokerCheck (brokercheck.finra.org): Search for Charles E. Lucius under CRD #1012912. BrokerCheck shows employment history, registrations, and any regulatory disclosures. Changes in status here could signal major career or firm-level shifts.

- SEC EDGAR (edgar.sec.gov): Look up Gradient Investments LLC under CIK 1542265. The firm's 13F filings show its holdings as an investment manager. Changes in AUM scale or reporting structure can affect fee revenue estimates.

- SECInfo and FilingExplorer: These third-party aggregators surface 13F-HR and N-PX filings from Gradient, giving you a view of filing frequency and any unusual reporting changes.

- Industry news sources covering the independent RIA sector: Any acquisition of Gradient Investments by a larger firm, a partial stake sale, or a strategic partnership would likely be covered in financial trade publications like RIAIntel, Financial Planning, or InvestmentNews.

Signals That Would Change the Estimate Significantly

- A reported sale or partial sale of Gradient Investments: Independent RIA acquisitions are common and well-documented. If Gradient sells or takes on a private equity partner, the equity value becomes realized and public.

- A major change in AUM: If the firm's reported AUM drops significantly (due to client losses, market conditions, or regulatory action) or jumps (from a major acquisition), the revenue-based valuation changes accordingly.

- New ownership disclosures in Form ADV: If the trust's 80% stake is restructured, reduced, or transferred, that would appear in the next ADV filing.

- Regulatory actions via FINRA or SEC: Any enforcement action or significant disclosure on BrokerCheck could affect both the firm's value and how confidence in the estimate is assessed.

- New business ventures or public appearances: If Lucius launches a new firm, takes a board seat at a public company, or makes a notable public investment, that would add new data points to the picture.

The most practical next step if you want the freshest possible picture is to pull the current Form ADV directly from SEC AdviserInfo, check the AUM figure, confirm the ownership trust is still listed at 80%, and then apply the same revenue-inference logic outlined above. That process takes about ten minutes and will get you closer to an evidence-based answer than any third-party net worth site.

One important framing note: 'estimated net worth' and 'confirmed net worth' are very different things. For a private business owner whose wealth is primarily tied up in a privately held firm, even a well-reasoned estimate carries meaningful uncertainty. The $5 million to $15 million range here is honest about that. If Gradient were ever sold or if personal holdings were ever disclosed, the actual figure could land anywhere in that range, potentially higher if firm valuations in the RIA space remain elevated, or lower if liabilities, distributions, or market conditions reduce the picture. Treat the estimate as a well-informed approximation, not a verified balance sheet.

FAQ

How can I update the estimate quickly if AUM or ownership changes after 2026?

If the goal is to reduce uncertainty, focus on the AUM number and the ownership percentage in the latest Form ADV, then re-run the revenue inference using a conservative fee rate band. The range can move several million dollars if AUM rises or if the firm’s fee schedule effectively shifts (for example, moving more clients into lower wrap-fee or institutional arrangements).

Why might a “net worth” estimate look high even if the owner is not sitting on cash?

The $5 million to $15 million range is not a statement about liquid cash. Because most value is tied to a private firm, your personal net worth proxy is heavily influenced by whether the firm’s equity is transferable, marketable, or subject to reinvestment and retained earnings, which is why sale-value scenarios can look higher than realized wealth.

What stops AUM-based revenue math from becoming an overconfident net worth number?

RIA “revenue” does not equal owner “net proceeds.” Operating costs, staff compensation, custody and platform costs, compliance expenses, and technology spending can materially reduce distributable profits. If you want a tighter estimate, you can bracket owner earnings by assuming typical RIA operating margins (without needing exact expenses).

How do I tell whether a one-number net worth claim is method-based or just a guess?

Third-party sites often show a single number because they implicitly pick assumptions for fee rate, margin, and liquidity. If their figure falls well outside the evidence-based band, it may reflect guessing about personal assets or using generic RIA valuation multiples without verifying the fee mix or current AUM.

Could the 80% trust ownership under- or overstate total wealth?

Yes. If the trust’s ownership remains at 80% but there are additional equity stakes, other entities, or cross-holdings not reflected in the ADV, the person’s total net worth could differ. Conversely, if liabilities are higher than expected at the firm or personally, the equity value may translate into less personal wealth than a simplistic valuation multiple suggests.

What would count as real evidence that some wealth became “realized” rather than potential?

If there were documented equity sales or strategic partner investments, those would not always appear as a public “sale of the business.” You may instead see indirect signals like changes in ownership structure in ADV amendments, entity name changes, or updated disclosures in regulatory records. Without those, assume no realized liquidity event has occurred.

Does the trust being revocable mean the net worth estimate is less reliable?

A revocable trust structure generally indicates estate-planning intent and often helps with probate avoidance, but it does not automatically tell you how much is distributed to beneficiaries. For net worth estimation, the key is whether the trust is still the controlling equity holder and whether any distributions are documented indirectly through changes in ownership records.

How would the net worth range change if Gradient Investments were sold?

If Gradient were ever sold, your estimate would shift toward the sale proceeds allocation, minus taxes, transaction costs, debt, and any reinvestment commitments. The current approach treats the valuation as potential, so any future transaction would require swapping multiples for a realized deal allocation.

What is the most common mistake people make when estimating net worth for private RIA owners?

One common mistake is mixing up “value of the firm” with “net worth of the person.” The firm valuation estimate can be used as a ceiling-like proxy for personal equity value, but your net worth would still depend on whether the owner has debt, guarantees, distributions, and non-firm assets that are not captured in public filings.

What sanity checks can I do to see if the estimate is internally consistent?

If you want to sanity-check the result, compare the implied owner earnings to typical CEO/major-owner compensation patterns in fee-only RIAs at that size, and check whether the estimated equity value aligns with how long the ownership has been held. A large mismatch usually signals that the fee rate, margin, or multiple assumptions are off.